Saving money during the holiday season can feel impossible. Between gifts, decorations, dinners, and travel, the costs add up fast. Most of us don’t suddenly earn more in December, so we have to find smart ways to stretch what we already have. That’s why we created this 15-day holiday money saving challenge. It’s designed to help you control holiday spending without cutting out the fun.

You don’t need a huge savings account or a complicated financial plan to make this work. Just follow these daily steps and watch the savings pile up.

While shopping for friends and family, it’s tempting to grab something for yourself. A cute sweater, a new gadget, a little treat; it all adds up. Before you check out online or in-store, take a moment to ask: is this for someone on my list?

To stick to your budget, avoid browsing for yourself entirely. Don’t click on targeted ads, and skip trying things on. Shopping for others is not an excuse to indulge in impulse buying.

Black Friday and Cyber Monday are known for deep discounts. But not all deals are good deals. Focus on high-value items that are truly discounted. Look for price drops on name-brand items, and buy them directly from the manufacturer when possible.

Be strategic: if you spot a big gift at a better price later in the season, some stores will let you price match. Check store policies, and don’t forget to use coupons or promo codes when available.

If you’ve ever heard of “Sober October,” the idea is simple: skip alcohol for the entire month. This challenge can be just as effective in December. Not only does it help you save money, but it’s better for your health, too.

Whether it’s wine with dinner or seasonal cocktails at parties, cutting out alcohol for a few weeks can save hundreds. Replace those drinks with festive mocktails or sparkling cider.

The best way to avoid overspending is to plan ahead. That starts with setting a holiday budget. Figure out how much you can spend overall, then divide that amount across categories like gifts, meals, travel, and decorations.

Even better, break it down by person. If you have a list of 10 people to shop for, decide what you’ll spend on each. Then stick to that number. No exceptions.

Normally, we don’t recommend paying only the minimum on credit cards or loans. But if your goal is to free up extra money this month, temporarily scaling back your debt payments might help.

Be careful: if you’re already making just the minimum payments, that could be a warning sign. In that case, consider getting help from a certified credit counselor. A debt management plan can lower interest rates and help you pay off debt faster in the long run.

Skip the streaming rental fees and visit your local public library instead. Most libraries offer free DVD rentals, including new releases and holiday classics. You can usually keep them longer than 24 hours and check out multiple movies at once.

Some libraries also have digital collections, letting you stream movies with a free library card. It’s an easy way to enjoy cozy nights in without adding to your bills.

Decluttering can be profitable. Look through your closets and drawers for clothes, shoes, electronics, or household goods you no longer need. Many consignment stores or resale platforms will offer instant cash or store credit.

If your items aren’t seasonally trendy, consider selling on community apps or local marketplaces. A few small sales can add up quickly and give you some extra money to work with.

-min.webp)

Holiday parties are fun, but expensive. If you’re usually the one hosting, it’s okay to take a break this year. Between food, drinks, and decorations, you could save hundreds by letting someone else take the lead.

If you still want to gather with friends, suggest a potluck or rotate hosting duties. You’ll still get the social time, without draining your wallet.

This can be one of the hardest steps. We all want to show love and appreciation, but buying gifts for everyone—friends, coworkers, neighbors—can get expensive fast.

Be intentional. Prioritize your immediate family and closest friends. For everyone else, consider writing heartfelt cards or giving small, homemade treats. A meaningful gesture doesn’t have to cost much.

If you’re part of a big group—like coworkers or a large family—consider suggesting a gift exchange. Secret Santa and White Elephant swaps are great ways to give and receive presents without overspending.

Set a spending limit, like $15 or $20. Everyone draws one name or brings one wrapped gift. You still get to enjoy the spirit of giving, but you’ll avoid having to buy for everyone individually.

Pair the event with a potluck or cookie exchange for even more holiday fun without the high price tag.

Homemade gifts can carry more meaning than store-bought ones. They also cost less and allow you to get creative. Make a batch of your favorite cookies or mix up spiced nuts, trail mix, or hot cocoa jars.

Pick up inexpensive tins or jars from a dollar store to package everything nicely. Add a ribbon or tag for a thoughtful, personalized touch. These kinds of gifts are perfect for neighbors, coworkers, or extended family members.

You don’t need a dozen dishes to make your holiday meal feel special. Choose one protein as the main course—like turkey, ham, or a vegetarian option—and build around it with a few sides.

If you’re hosting, let guests contribute. Most people are happy to bring a dish or dessert. It keeps costs down and gives everyone a chance to share a family recipe or favorite treat.

If you’re looking for more inspiration, read How to Do Thanksgiving on a Budget for practical tips you can use for any holiday meal.

Retailers compete fiercely during the holidays. That means you may be able to get the lowest price available without running from store to store.

Before you buy anything, check if the store offers price matching. Many stores will match a competitor’s price on the same item. All you have to do is show the lower price on your phone or printout at checkout.

This works especially well for big-ticket items like electronics, toys, and appliances... some of the most common holiday purchases.

Never shop online or in-store without checking for coupons first. It only takes a few seconds to do a quick search, and it can save you a lot.

Some stores offer printable coupons, while others have mobile apps filled with deals. Browser extensions can automatically apply promo codes at checkout. You can also sign up for store emails in exchange for a one-time discount.

Many grocery stores also offer seasonal promotions. Use coupons to stock up on items for your holiday menu or snacks for road trips and gatherings.

Shipping costs can explode if you wait until the last minute. Carriers charge a premium for overnight or expedited shipping, especially in December.

Plan ahead and get your packages in the mail at least two weeks before the big day. You’ll have more options, pay less, and avoid the stress of wondering if your gift will arrive on time.

Better yet, ship directly to the recipient using the store’s free or discounted shipping offers when available.

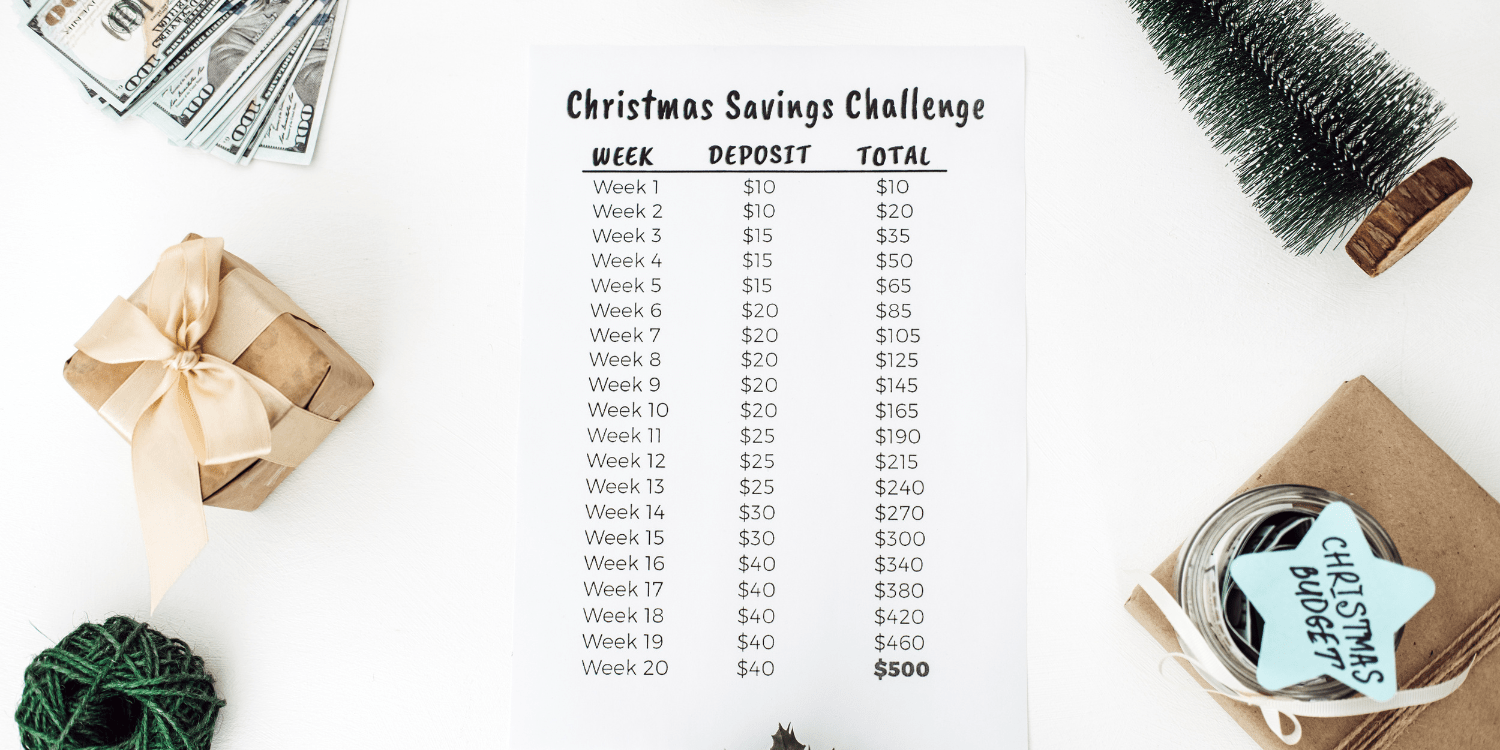

Even if you’re coming into this season with little saved, now is a great time to think about next year. A savings account just for holiday expenses can help you build a small buffer over time. Start by setting aside $10 or $20 a week beginning in January. By the time the next holiday season rolls around, you’ll have a helpful cushion.

To stay consistent, use automatic transfers or apps designed for saving challenges. Some people enjoy using a saving challenge book or printable tracker to stay motivated.

If you’re interested in building stronger financial habits, the Emergency Fund guide from the CFPB is a good place to start. It’s a valuable year-round resource, not just for the holidays.

When you’re working with a tight budget, using debit cards can help keep you from overspending. Because you’re limited to the money already in your checking account, it’s easier to stick to your holiday spending goals.

Some banks even offer features like round-up savings, where every purchase is rounded up to the nearest dollar and the difference goes into a savings account. Check your bank’s offerings to see if you can benefit from these automated savings tools.

Nothing busts a budget faster than panic shopping. When you’re out of time and ideas, it’s easy to overspend on whatever is available. This usually means paying full price, plus extra for gift wrap, fast shipping, or rush pickup.

Instead, plan ahead, even by just a week or two. Create a shopping list, set your budget, and buy gifts early. You’ll be more relaxed, more thoughtful, and more in control.

If you’ve made it through all 15 days of this holiday saving challenge, congratulations! These money saving challenges are about more than short-term wins; they’re about shifting your mindset. Saving doesn’t have to mean sacrifice; it can simply mean making smarter choices.

Look back on what worked best for you. Maybe you enjoyed making personalized gifts. Maybe you realized that your budget could stretch further with just a little planning. The key is to take these wins and carry them forward into the new year.

You’ve proven you can save money during the most expensive time of the year. Now imagine what you can do the rest of the year with the same tools and focus.

If you liked the daily challenge format, consider turning it into a habit. Create your own saving challenge book or journal where you track financial goals, set mini-challenges each month, and record your progress.

Your book doesn’t have to be fancy. Use a notebook, printable template, or spreadsheet. The goal is to stay consistent. Some people try challenges like “No-Spend January” or “Cash-Only Weeks” to reset their finances after the holidays.

Try pairing your book with a dedicated savings account. When you meet a challenge goal, reward yourself by transferring money into your account right away. It helps build positive momentum and keeps you motivated.

One of the best uses for any money saved during this challenge is starting or growing your emergency fund. If you avoided hosting a party, cut back on drinks, or stuck to a gift budget, that extra cash shouldn’t just sit in your checking account.

Open a separate savings account for emergencies, if you don’t already have one. Even $100 set aside for unexpected expenses can be a lifesaver. Over time, aim to build up at least three months’ worth of living expenses.

If you’re not sure how to begin, the CFPB’s guide to emergency savings (linked above) is an excellent step-by-step resource.

This challenge isn’t just for adults. Get the whole family involved next year. Assign your kids their own mini-saving goals or holiday tasks, like finding coupon codes or wrapping gifts with homemade materials.

Saving money becomes easier when it’s part of your household routine. Children especially benefit from learning these habits early on. Helping them understand wants vs. needs, delayed gratification, and budgeting will serve them well for years to come.

Explore more family-focused ideas in our "Raising a Money Smart Child" workbook, which highlights creative, goal-based financial learning. Find it among our free financial education guides. Another free tool is the Money Smart program for young people from the FDIC that can help teach kids and teens core financial skills.

Manual saving challenges are great, but they’re even better when supported by automation. Consider pairing your saving goals with tools like:

Using these features helps take the pressure off, especially after the holidays when energy and focus may dip.

With the holidays behind you, now is a great time to plan your next step. Maybe that’s creating a full household budget, tackling credit card debt, or starting a sinking fund for next year’s expenses.

Use what you’ve learned from the challenge to shape your approach. What spending surprised you? What felt easy to skip? What could you do differently next year?

To keep the momentum going, try taking a look at our New Year’s Debt Resolution Tips, which lays out practical ways to reduce your debt faster and stay financially focused in January.

Saving during the holidays doesn’t mean you have to miss out. By using thoughtful planning, a bit of creativity, and some daily discipline, you can stretch your dollars and still celebrate fully.

Let this challenge be your stepping stone toward better money habits. Whether you start building an emergency fund, use a savings account to plan for next year, or simply spend more mindfully, every small step counts.

If you’re ready to take your next step, we’re here to help.

Whether you’re dealing with credit card debt, setting up a budget, or looking to create long-term financial stability, Credit.org has free tools and counseling services to help.

Get started today with a free one-on-one session with a certified credit counselor.