When you’re applying for a mortgage, it’s important to know if your loan might be classified as a HOEPA loan. HOEPA stands for the Home Ownership and Equity Protection Act, a federal law designed to protect consumers from unfair lending practices—especially with high-cost or high-fee loans.

But HOEPA doesn’t apply to every type of mortgage. Knowing which loans are covered under HOEPA—and which ones are not—can help you understand your rights, ask the right questions, and avoid risky lending.

This article explains the loans that fall under HOEPA coverage, which loans are excluded, and what protections the law offers to consumers.

The Equity Protection Act was added to the Truth in Lending Act (TILA) in 1994. It was a direct response to abusive practices in the subprime lending market. Before this law, many homeowners were being taken advantage of by predatory mortgage lending, especially in home equity loans and refinances that stripped away their home’s value.

HOEPA was created to stop that. The law applies to certain loans that meet thresholds for interest rates, points and fees, or prepayment penalties. If a loan passes any of those limits, it becomes a HOEPA-covered loan and must follow strict rules.

Not every expensive loan is covered by HOEPA. Specific standards must be met. These include:

If the loan’s annual percentage rate (APR) is too high—typically a certain number of percentage points above the average prime offer rate (APOR)—it may be considered a high cost mortgage.

HOEPA coverage applies if points and fees exceed a specific percentage of the loan amount. This includes charges like:

For most loans over $25,000, the fees threshold is 5%. For smaller loans, the threshold may be 8% or more.

If the loan includes prepayment penalties that last longer than 36 months or cost more than 2% of the loan amount, it could fall under HOEPA.

These rules are updated yearly by the Federal Reserve and Consumer Financial Protection Bureau (CFPB). If your loan triggers any one of these thresholds, it is a high cost mortgage subject to HOEPA coverage.

-min.webp)

Let’s break down the specific types of loans that are covered under the equity protection act HOEPA:

These loan types are most likely to be high-cost, particularly when marketed to borrowers with poor credit or limited financial knowledge.

If your loan is covered under HOEPA, the lender must:

Now let’s look at the loans that HOEPA specifically does not cover. Even if these loans are high-cost or complex, they may fall outside the law’s coverage:

Knowing these exclusions is essential. Just because a loan isn’t HOEPA-covered doesn’t mean it’s safe—it means different rules apply.

One of the most critical protections added by the Consumer Protection Act and later expanded by the Dodd-Frank Actis mandatory pre loan counseling for high-cost loans. If your loan meets the criteria for HOEPA, you must speak to a HUD-approved housing counselor before the loan can close.

This counseling is designed to:

You can find a list of approved counselors at HUD.gov or use Credit.org’s counseling services for personalized guidance.

HOEPA helps consumers stay in their homes, avoid foreclosure, and reduce the chances of being trapped in alternative mortgages with unaffordable terms. It protects first-time homebuyers, first-generation buyers, and anyone vulnerable to unfair loan practices.

This law is especially relevant for:

Understanding what’s covered by HOEPA—and what’s not—gives you a stronger foundation for long-term home ownership and financial security.

The Dodd-Frank Act, passed after the 2008 financial collapse, made major changes to how mortgage lending is regulated. One of its key impacts was expanding HOEPA’s authority. Before Dodd-Frank, HOEPA only applied to a narrow range of loans. Today, more types of high cost mortgage loans fall under its coverage.

Key enhancements include:

The Dodd-Frank reforms reinforced the purpose of HOEPA: to prevent abusive mortgage lending practices and give borrowers a fair shot at sustainable home ownership.

HOEPA regulates the mortgage lending industry by imposing specific rules on how lenders interact with borrowers. A key part of this regulation is limiting how fees paid, interest rates, and other costs are structured on loans.

For HOEPA loans, lenders are prohibited from:

These requirements help protect consumers from deceptive or predatory mortgage lenders. Lenders that ignore these rules may face serious consequences, including fines, lawsuits, and forced loan rescission.

Each year, the Federal Reserve, working with the Consumer Financial Protection Bureau, publishes updated thresholds that determine HOEPA status. These include:

To avoid triggering HOEPA, lenders must structure loans carefully. For consumers, this means reviewing all disclosures carefully and understanding the full cost of the loan—including monthly payment, long-term interest rate, and total loan amount.

To check the latest thresholds, visit the CFPB’s official Regulation Z resource.

While HOEPA offers strong protections, some lenders still try to skirt the rules or trick borrowers into risky loans. Watch out for these abusive practices:

These tactics are often used against borrowers with limited experience or low credit scores. That’s why pre loan counseling and working with trusted homeownership counseling organizations is essential.

Learn 11 Tips for Avoiding Predatory Lending

If you’re offered a HOEPA-covered loan, the law requires you to go through obtain homeownership counseling. This step can’t be skipped—even if you think you understand the loan terms.

Counseling ensures:

HUD maintains a list of approved agencies, but Credit.org also offers housing and mortgage counseling to guide borrowers through the application process.

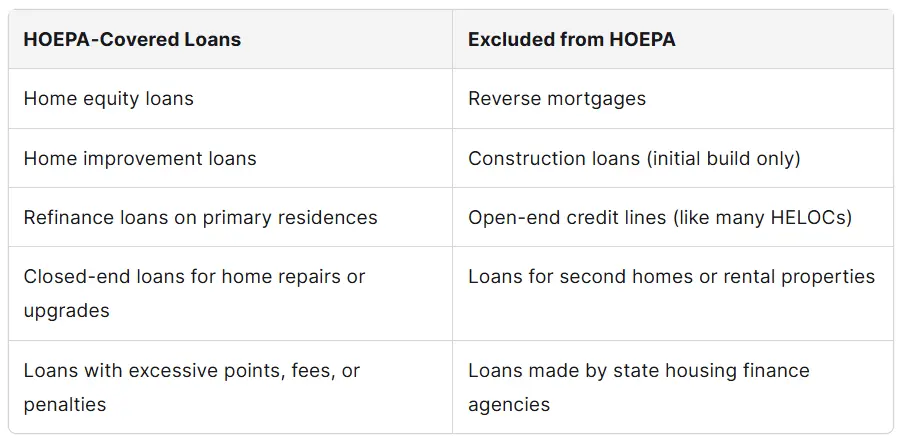

Here’s a side-by-side breakdown to help clarify which loans are HOEPA-covered and which are excluded:

Understanding these distinctions is critical. A loan that doesn’t fall under HOEPA can still be risky—just with different regulations. Always look closely at the loan terms, and compare costs against the points and fees threshold.

HOEPA is more than just a list of rules. It’s part of a larger movement to protect consumers, improve transparency, and hold mortgage brokers and lenders accountable.

Other laws that work together with HOEPA include:

These rules apply whether you’re buying your first home, refinancing an existing loan, or considering alternative mortgages like adjustable-rate loans.

Learn more about Consumer Credit Acts and Laws to Protect You

If you’re applying for a mortgage and think it might qualify as a high cost mortgage loan, take these steps:

Whether you’re looking at a purchase money mortgage or a home equity mortgage loan, understanding your rights can help you protect your home ownership and avoid costly mistakes.

If you need help understanding any aspect of your mortgage loan, get HUD-approved housing counseling today.