If you often wonder where your money went at the end of each month, you’re not alone. Many people struggle with spending habits that quietly chip away at their savings, financial goals, and long-term stability. The good news is that with a few small changes and greater awareness, you can break the cycle of bad spending habits and create a healthier financial future.

In this guide, we’ll explore practical steps you can take to improve your money habits, avoid financial stress, and finally stop spending money on things that don’t serve your bigger goals.

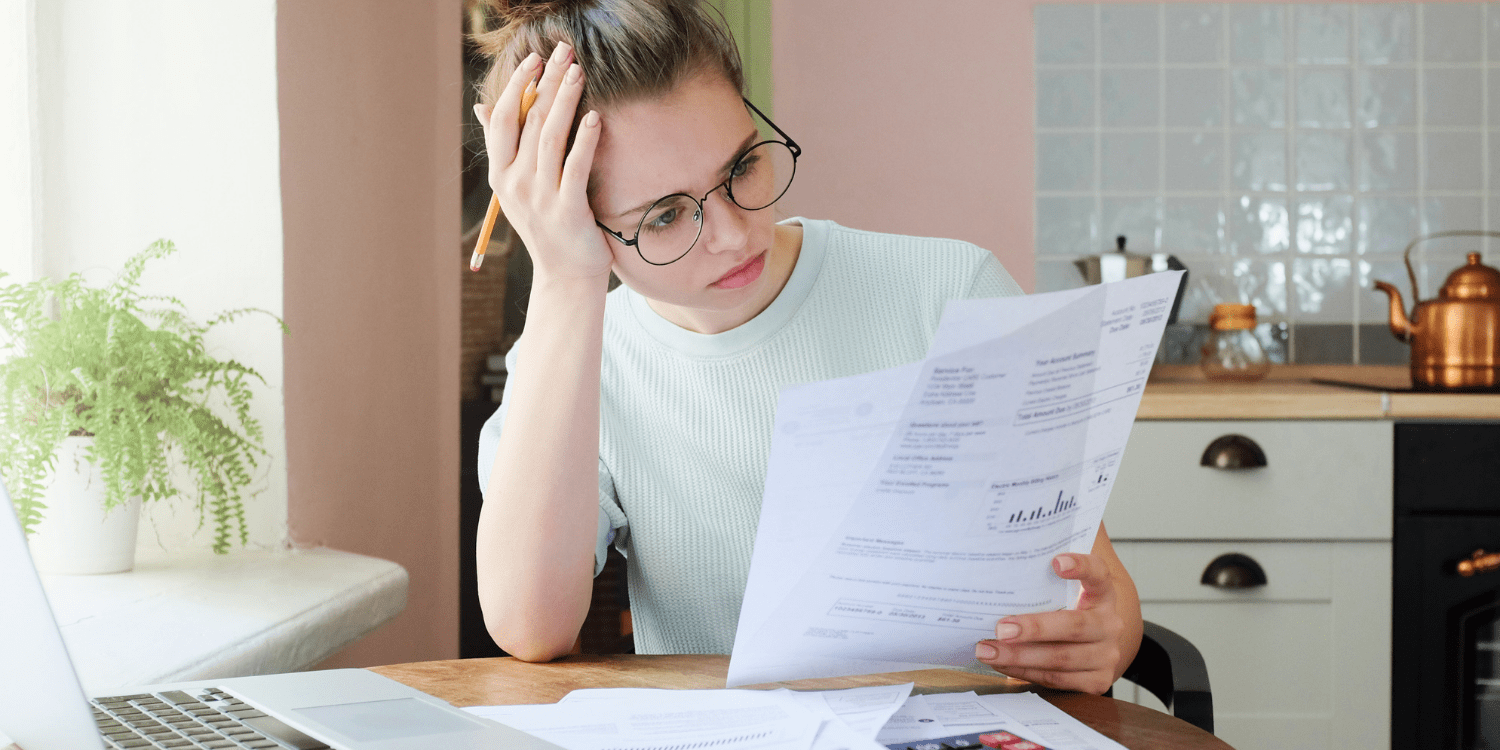

Before you can fix your financial problems, you need to understand what’s causing them. Bad spending habits often sneak into your life gradually and may seem harmless at first. But over time, they can build up, draining your savings and putting you deeper into debt. The first step toward positive change is to recognize the patterns that are holding you back.

Here are some of the most common bad spending habits to look out for:

Identifying these behaviors doesn’t mean you’ve failed; it means you’re ready to take charge. Once you know where the problems are, you can build better habits that support your financial goals.

Unchecked spending affects more than your bank account. It can create emotional stress, lead to unnecessary debt, and make it harder to reach savings goals. Even small expenses, when added up over weeks and months, can stand between you and your ability to save for emergencies, retirement, or even next month’s bills.

Building financial health means thinking ahead, tracking your habits, and making better day-to-day choices that support your long-term stability.

Impulse buying is one of the most common spending problems. It’s when you buy something suddenly, without planning or comparing prices, often driven by emotion or environmental cues. According to Wikipedia, impulse purchases are typically unplanned and influenced by external triggers like packaging, placement, or discounts.

To stop impulse buying, try these strategies:

For more long-term strategies, check out 20 Household Habits to Save Money.

Keeping a spending journal or using a budgeting app can help you see patterns in your behavior. Are you more likely to spend money on weekends? Do you shop when you’re stressed? Are you unaware of how much you’re spending on coffee or delivery fees?

Tracking your spending gives you a sense of control and helps you decide where to cut back. You can also better plan for upcoming expenses like car maintenance or back-to-school supplies.

Spending money is easier to manage when you know what you’re working toward. Set clear goals like:

Put these goals somewhere visible to keep them top of mind. Once you have a purpose, it’s easier to stick to your plan.

A realistic budget is your best defense against overspending. Use your monthly after-tax income to determine how much you can safely spend on needs, wants, and savings. Start by covering fixed expenses like rent, utilities, and minimum debt payments. Then allocate money toward savings accounts and flexible categories like groceries or entertainment.

To get started, explore our Essential Household Budgeting Tips and review this CFPB guide to creating and sticking with a budget for additional help.

One of the simplest ways to stop spending money is to separate your actual needs from your wants. Needs include rent, utilities, groceries, and healthcare. Wants are things like clothes you don’t need, gadgets, or restaurant meals.

Before you make a purchase, ask yourself:

Just a moment of reflection can save you hundreds over time.

Subscription fatigue is real. Streaming services, delivery memberships, digital apps, and newsletters can quietly drain your finances. Do a monthly check-in on all recurring charges. Cancel any services you no longer use or can share with a family member.

It’s easy to swipe a card without thinking, especially for small expenses. But credit cards can turn convenient purchases into long-term debt. Avoid carrying balances whenever possible, and always pay more than the minimum amount on your credit card bill.

If you’re struggling with debt, explore credit counseling services to create a repayment plan that works for your situation.

It’s not always the big purchases that cause problems; small, frequent spending often flies under the radar. Things like snack runs, app upgrades, or frequent coffee trips can add up quickly.

Try a one-week “no spend” challenge and track how much you save by cutting small expenses. Then redirect that money into your savings account.

Having separate accounts can make a big difference. Keep your spending money in a checking account and use a savings account for longer-term goals. This makes it harder to accidentally dip into money meant for emergencies or retirement.

Look for high-yield savings accounts that offer better interest rates than traditional banks.

Discretionary spending includes things like entertainment, fashion, and hobbies. While these aren’t bad in moderation, they can quickly spiral out of control. Set limits for how much you’ll spend in these categories and track them weekly.

Without emergency savings, every surprise becomes a crisis. Aim to build a fund of at least $500 to start, then work toward covering three to six months of essential expenses. Even small weekly contributions will grow over time.

For more ideas on how to grow your savings, check out our guide on how to start an emergency fund to prevent debt.

Avoid impulse purchases by making a shopping list and sticking to it. If you know a big purchase is coming up, like a new appliance or holiday gift, start setting money aside in advance. This helps you avoid debt and stay within your budget.

Set up automatic transfers from your checking to your savings account. Even $10 a week can make a difference. This approach takes the pressure off and turns saving into a habit.

Whether you’re saving for retirement, a down payment, or a family vacation, having a clear goal can help you stay motivated. Write it down, track your progress, and celebrate milestones along the way.

Making a few poor spending choices doesn’t mean you’ve failed. Financial wellness is a journey, not a destination. The important thing is to become more aware and make better decisions going forward.

Improving your financial health doesn’t mean giving up all fun or never making a splurge again. It means knowing when, where, and how to spend money in ways that serve your goals and values.

To make the most of your efforts, remember to:

If you’re ready to change your financial future, we’re here to help. Credit.org offers free one-on-one credit counseling, personalized debt relief, and housing support to guide you toward better money habits and long-term financial wellness.

Take the first step today. Talk to a nonprofit financial counselor and start creating a plan that works for your life.