Understanding how debit and credit cards work can help you make smarter financial choices. Even though both cards often look the same, they are very different tools. From fraud protection to how they affect your credit score, it’s important to know which card to use and when. Make sure to understand your billing cycle and avoid paying interest by paying off the balance. In case of credit transactions gone wrong, this protection is crucial. Responsible credit card use, including paying your credit card bill on time, supports a strong score.

A debit card is connected directly to your checking account. When you use it, the money comes out right away. This makes it a great tool for keeping track of your spending. You can only use the money you already have, so you’re less likely to go into debt. This is often the default cash account for debit card transactions. A debit card transaction reduces your available balance immediately.

Debit cards are often used for everyday purchases, like groceries or gas. You can also use them to get cash back at the register. This can help you avoid ATM fees, which are often expensive.

However, debit cards don’t offer the same level of security as credit cards. If someone steals your debit card, they can access your money directly. You must act fast to protect your account. According to the Consumer Financial Protection Bureau, your loss is limited to $50 if you report a stolen debit card within two days. After two days, your loss could go up to $500. If you wait more than 60 days, your bank may not cover the loss at all (source).

Credit cards let you borrow money to make purchases. Instead of using your own funds, you are spending the bank’s money and paying it back later. This gives you more time to pay for large items or handle emergencies.

One of the biggest advantages of using a credit card is fraud protection. If someone steals your credit card or your card number, you are not legally responsible for most of the charges. Federal law limits your liability to $50. In many cases, your credit card company won’t even charge you that. Monitoring your billing cycle and using your credit card responsibly helps prevent issues.

If you run into a problem with an online purchase, the type of card you used matters. When an item never arrives or shows up damaged, credit cards give you more leverage. The charge can usually be disputed before the money fully leaves your account. With a debit card, the funds are pulled immediately, and recovering them can take time, if it happens at all. That extra layer of protection is one reason credit cards are generally safer for online purchases and higher-risk transactions.

The rules that govern these protections are not informal. Credit card users have defined rights under federal law. The Federal Trade Commission explains those protections in plain language at FTC.gov.

A credit card works by temporarily shifting the payment responsibility to the card issuer. When you make a purchase, the bank pays the merchant on your behalf. You receive a statement later showing what you owe and when payment is due. If you pay the full balance by that date, no interest is charged. If you carry a balance, interest begins accumulating on the unpaid portion.

This is where many people run into trouble. Paying only the minimum keeps the account current, but it also stretches the debt out over time and increases the total cost through interest. Credit cards can be useful for managing cash flow, but high interest rates and late payments can quickly undermine that benefit and damage your credit score.

Some cards also offer rewards, such as cash back or travel points. Used carefully, rewards can be a modest perk. Used carelessly, they become an incentive to overspend. The math only works in your favor if the balance is paid in full each month.

Outside of everyday spending, the words “debit” and “credit” come from accounting, where they describe how transactions are recorded rather than how consumers pay. A debit typically reflects a decrease in an asset or an increase in an expense. A credit often represents an increase in a liability or a reduction in an expense. These rules are how financial institutions keep their books balanced.

For example, when you use a debit card at a grocery store, funds move directly out of your bank account. When you use a credit card, the transaction creates a balance you owe, which is recorded differently behind the scenes. These entries are part of a system called double-entry accounting, often shown using T-accounts.

You do not need to master accounting to manage personal finances. Still, understanding that “debit” and “credit” have technical meanings beyond consumer cards can make financial statements and account activity easier to interpret.

An asset account is anything you own that has value. This includes your checking and savings accounts, property, or anything else that could be turned into cash. When you deposit money into your checking account, you’re increasing your assets.

Both debit and credit cards affect your asset accounts in different ways. Debit cards reduce your assets right away since the money comes directly from your account. Credit cards don’t touch your assets immediately; instead, they create a debt that you have to pay later.

Learn more from Credit.org: Basics of Banking

.webp)

An expense account tracks the money you spend. In accounting terms, it includes things like groceries, bills, rent, or entertainment. When you use a debit card, the money comes out of your account right away, so you can easily see how much you’ve spent. This can help you manage your expense accounts more closely and stay on budget.

With credit cards, your spending is recorded, but the actual money doesn’t leave your account until later. This delay can make it harder to keep track of your expenses if you’re not checking your balance regularly. That’s why it’s important to monitor your credit card account online or through a mobile app.

An equity account shows your ownership in something, such as the value of your bank account after all debts are subtracted. Equity represents what you truly own. For example, if you have $1,000 in savings and no debt, that’s your equity.

Using a debit card reduces your equity immediately because you’re spending cash you already own. Using a credit card doesn’t affect your equity right away, but if you don’t repay your balance, your equity can go down as you build up debt and interest.

Understanding the difference between asset, equity, and expense accounts can help you keep your finances in order. While you don’t need to be an accountant, knowing where your money goes is a powerful step toward financial health.

One of the most important benefits of using a credit card is that it can build credit. Every time you pay your credit card bill on time, that payment is reported to the credit bureaus. Over time, this shows lenders that you are responsible with money.

A good credit score helps you qualify for better interest rates on loans, lower insurance premiums, and even housing. Debit card use, on the other hand, is not reported to the credit bureaus and does not help build your credit history.

If you’re just starting out or have had credit trouble in the past, a secured credit card can help you rebuild your credit. These cards require a deposit that becomes your spending limit. Over time, responsible use can lead to better credit opportunities. Credit.org offers help with credit on demand.

Many people use credit cards because they allow you to earn rewards. Depending on the card, you might get:

These programs can be valuable if used wisely. If you pay off your balance each month, you’re getting benefits for money you would have spent anyway. But if you carry a balance, the interest can outweigh the value of the rewards. Always check the terms of the rewards program to make sure it fits your lifestyle.

Debit cards usually don’t offer rewards, which is another reason some people prefer to use credit cards for their purchases.

Fraud protection is one of the biggest reasons experts recommend using credit cards instead of debit cards, especially online. If someone uses your debit card fraudulently, the money leaves your account right away. Even if you report the theft quickly, it can take time for your bank to investigate and return the funds.

Credit cards, on the other hand, offer more robust protection. As mentioned earlier, you’re only liable for up to $50 in unauthorized charges. Many card issuers offer zero-liability policies, meaning you pay nothing for fraudulent activity.

Credit cards also give you leverage when something goes wrong with a purchase. If an item never arrives or shows up damaged, you can ask the card issuer to pause or reverse the charge while the issue is reviewed. With debit cards, the money typically leaves your account right away, which limits your options if a dispute drags on. That difference matters most for online purchases and transactions where the seller is unfamiliar.

For practical guidance on protecting your accounts and personal information, the Federal Trade Commission maintains a clear overview at https://consumer.ftc.gov/identity-theft-online-security.

The better question is not whether debit or credit is “better,” but when each makes sense. The right choice depends on the type of purchase and how you typically manage cash flow.

Debit cards tend to work best when you want spending to stay tightly tied to the money you already have, such as for small, routine purchases or when getting cash back at the register. They can also be useful if avoiding debt entirely is a priority.

Credit cards make more sense when there is greater risk or a longer timeline involved. Online purchases, travel expenses, and situations where fraud protection matters are common examples. They can also help build credit, but only if balances are paid in full and on time.

Credit cards influence more than just a single purchase. Used carefully, they can add flexibility and security. Used poorly, they can create persistent financial strain.

Carrying a balance means interest starts accumulating, often at relatively high rates. Even a modest balance can grow faster than expected if only minimum payments are made. Over time, interest costs can exceed the original purchase amount.

Payment timing also matters. Late payments affect your credit score, and payment history is the most heavily weighted factor. Consistently paying on time does more for long-term credit health than almost any other habit, and it avoids late payment fees.

Most credit cards come with potential fees that are easy to overlook, including annual fees, late fees, cash advance charges, and foreign transaction fees. Some cards waive annual fees, while others charge them in exchange for rewards or benefits. Reading the terms carefully helps ensure the card fits how you actually plan to use it.

Debit cards generally involve fewer fees, but they are not fee-free by default. Out-of-network ATM use or overdrafts can still trigger other charges or overdraft fees. Keeping track of your balance is essential to avoid unexpected costs.

Every credit card has a borrowing limit, which is based on factors such as income, credit history, and prior payment behavior. Limits may increase over time with responsible use, but using too much of that available credit can work against you.

Carrying high credit balances relative to your limit can lower your credit score. A common guideline is to keep balances below roughly 30% of available credit. Staying well under the limit signals control and reduces risk in the eyes of lenders.

Debit cards place a natural cap on spending by restricting purchases to available funds. That can help prevent overspending, but it also means large or unexpected expenses require savings to be available upfront.

Both debit and credit cards now include built-in security features designed to reduce fraud. These often include EMV chip technology, contactless payments, multi-factor authentication for online transactions, and real-time alerts for unusual activity. While no system is perfect, these tools make it easier to spot problems early and respond before damage spreads.

Still, fraud protection is typically stronger with credit cards. You can turn off your card using a mobile app, freeze your account if needed, and often get updates when unusual activity is detected.

Debit cards also have fraud monitoring, but since they access your real money directly, the risk of loss is higher. It’s important to act quickly if you lose your card or notice unauthorized charges.

Learn more from Credit.org: 7 Things a Credit Card Can Do That Debit Cards Can't

If your credit card is lost or stolen:

Federal law limits how much you can be held responsible for unauthorized credit card charges, and many issuers go further with zero-liability policies. As long as you report suspicious activity promptly, you generally are not on the hook for fraudulent purchases.

Debit cards work differently. If a debit card is stolen, time matters much more. You should contact your bank right away so they can freeze the account and issue a replacement card. In some cases, you may also be asked to file a police report. While the bank investigates, keep a close eye on your account for additional withdrawals or charges.

Depending on how quickly you act, you could still be responsible for some of the missing funds. That delay risk is one reason credit cards tend to offer more peace of mind for large purchases or online transactions.

Preventing Identity Theft

Reducing fraud risk starts before anything goes wrong. Credit.org offers a Free Course on Identity Theft Prevention that walks through practical steps for protecting personal information and responding if your data is compromised.

Government Help with Card Fraud

Federal resources can also help if fraud occurs. USA.gov maintains a dedicated page on scams and fraud at https://www.usa.gov/stop-scams-frauds, with guidance on reporting lost cards, disputing unauthorized charges, and navigating recovery after identity theft.

Despite the added protections that come with credit cards, debit cards still serve an important role. For many people, they provide a straightforward way to spend only what is already available and avoid accumulating debt.

Debit cards are often a better fit for routine purchases such as groceries or fuel, situations where you want tighter spending limits, or when cash back at the register is convenient. They can also be useful if you are not yet eligible for a credit card or prefer to keep spending closely tied to your checking balance.

Because you’re spending your own money, there’s no interest to worry about and no risk of debt. For people who are just starting to manage their money or recovering from credit problems, debit cards are a safe and simple option.

Using a debit card can make it easier to follow a budget. Many banks offer tools to help you track your spending by category. This helps you understand where your money is going and what you can cut back on.

For families or individuals on a strict monthly budget, using only debit cards is one way to make sure you don’t spend more than you earn. You can even set up text alerts or mobile notifications to let you know when your balance is getting low.

Many parents start teaching their teens about money by giving them a debit card tied to a student account. This helps young adults learn how to manage spending without the risk of debt.

As they grow older and learn to manage money well, they can move on to using a credit card. Starting with a secured card can help young people build their credit safely, with a limit based on a deposit they provide.

Prepaid debit cards are another option for people who don’t have a bank account or who want tighter control over their spending. These cards are loaded with a fixed amount of money, and you can only spend what you’ve added.

However, prepaid cards often come with fees, such as monthly service charges or ATM fees. If you choose to use one, read the terms carefully and shop around for the best deal.

While debit cards are great for everyday use, credit cards can be helpful in emergencies. Whether your car breaks down or you need to pay for unexpected travel, having available credit can help you cover the cost and buy time to repay.

Still, it’s important to have an emergency savings fund so you don’t have to rely solely on credit. Credit cards are a backup, not your primary safety net.

Many people carry both a debit and a credit card. The key is knowing when to use each:

By using both cards wisely, you can protect your finances, build credit, and stick to your budget.

Whether you use a debit or credit card, keeping an eye on your accounts is essential. Check your transactions often, either through mobile apps or online banking. Set up alerts for large purchases or foreign transactions to stay informed.

Also review your credit report at least once a year. You can get a free copy from all three major credit bureaus at AnnualCreditReport.com, a government-approved site. This can help you catch fraud or errors early.

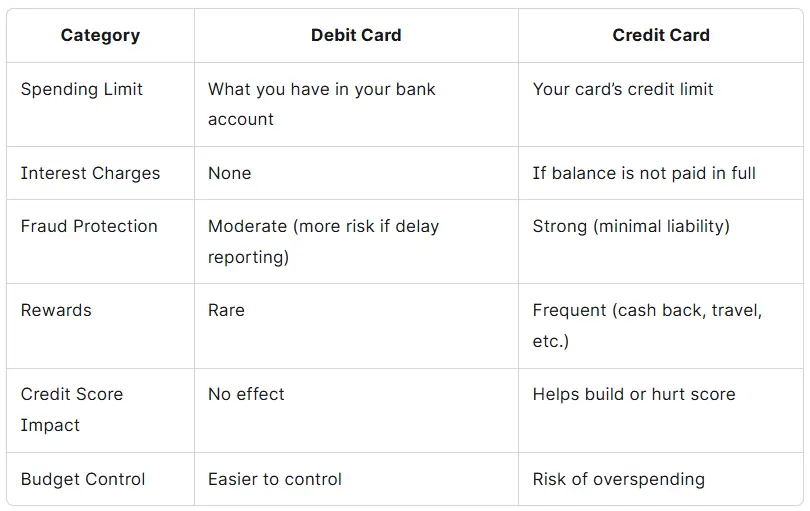

Here’s a quick breakdown:

Adding up all of the above, both credit and debit cards have their advantages. Most experts advise using credit instead of debit unless you’re getting cash back, but debit cards are the more popular option these days.

If you’ve been using credit and have gotten into too much debt, call us for a free confidential counseling session. We’ll help you create a plan to conquer your debts and achieve financial freedom.