Buying your first home is exciting, but the home buying process can feel overwhelming. This simple guide explains who the lenders are, what they offer, and how you, especially first time buyers with limited savings, can find the right first time buyer mortgage in 2025.

Pro Tip: Always ask for a Loan Estimate from at least three lender types. It shows exact monthly payments, loan amount, and all other costs side by side.

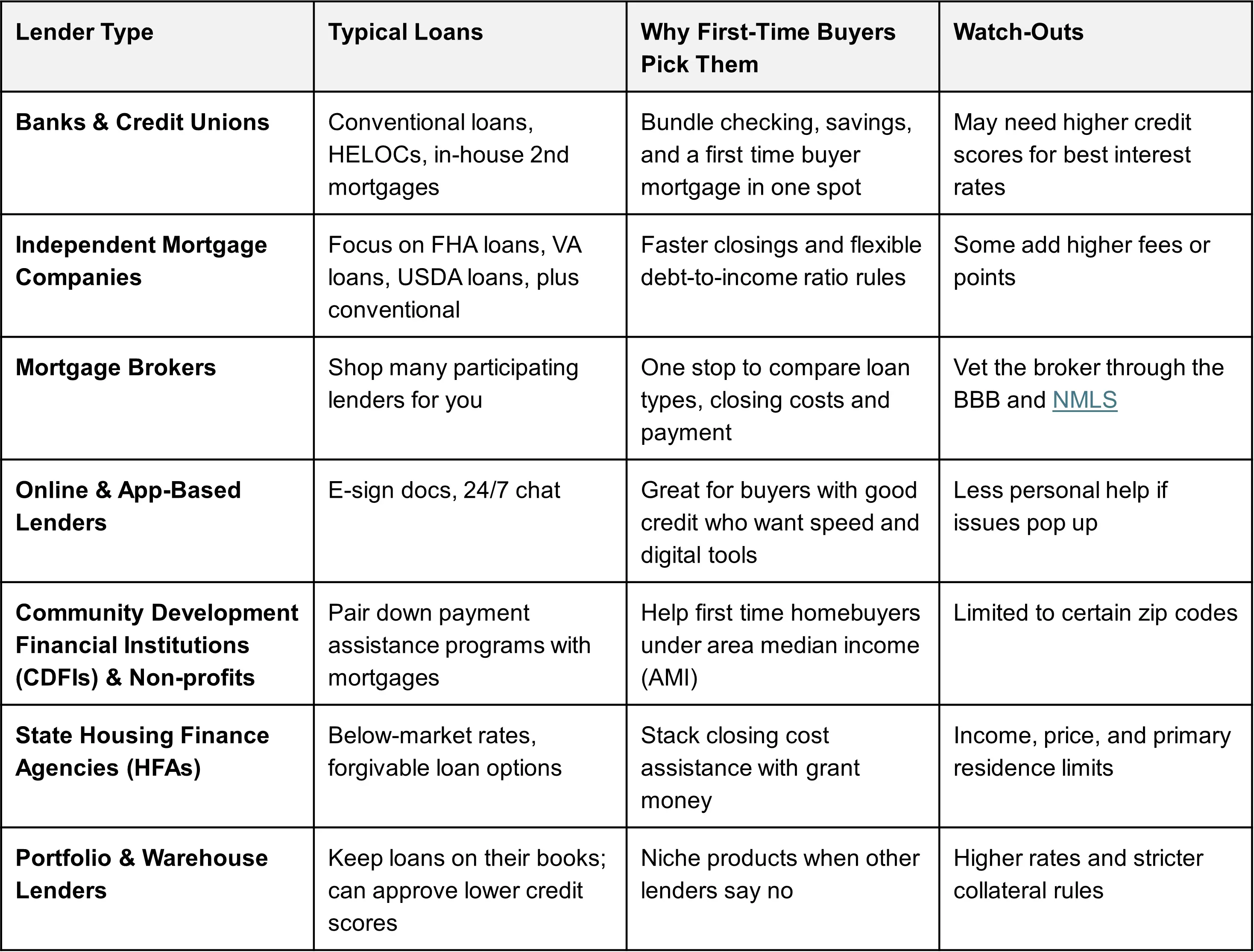

These lenders hold your loan and your paycheck. If you have good credit and stable income, they may knock 0.125 % off your rate or waive some closing costs for keeping direct deposit.

Sometimes called “non-bank lenders,” they write most first time homebuyer loans today, including new FHA loan limits of up to $524,225 (regular areas) and $1,209,750 (high-cost) in 2025.

Brokers act as match-makers, not money sources. They collect your docs once, then shop banks, credit unions, and wholesale lenders for the best fit. Bankrate notes they shine when you need down payment flexibility or a quick “rate lock.”

-min.webp)

Think “apply on your phone at 10 p.m.” Many cut paperwork time in half. Check reviews and compare interest rates before you hit “submit.”

Groups like local housing funds bundle assistance programs, financial coaching, and homebuyer education. If your income falls below county guidelines, you may score a 0 % 2nd mortgage that wipes out after ten years. Learn more from our favorite CDFI, Springboard Home Loans.

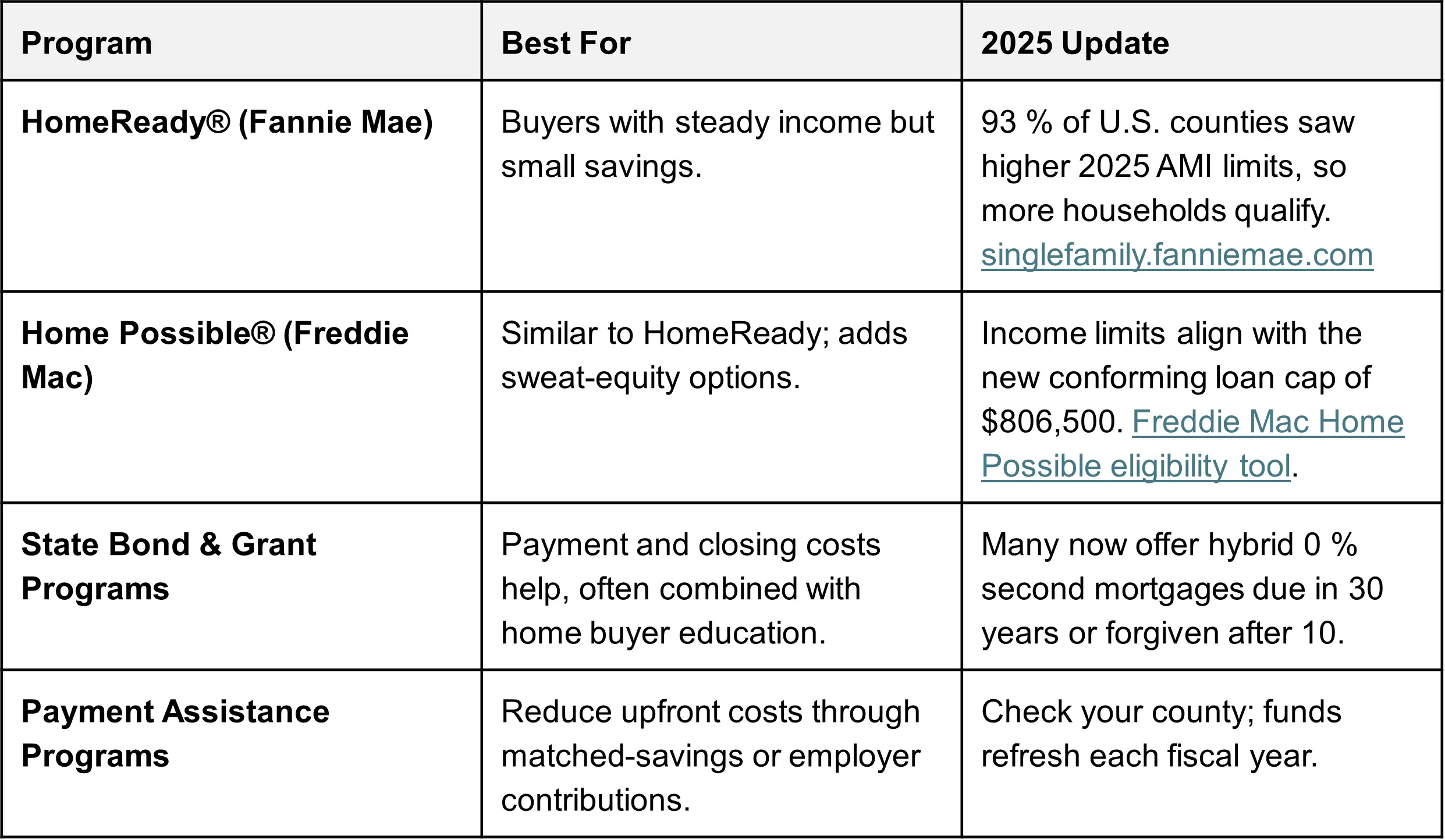

Every state has an HFA. They partner with Fannie Mae and Freddie Mac to offer HomeReady or Home Possible loans plus grant money for closing cost assistance. Check your state’s 2025 income chart and list of eligible buyers.

These lenders keep loans rather than selling to investors. Good match if you need a jumbo loan amount, own a unique property, or have a short job history.

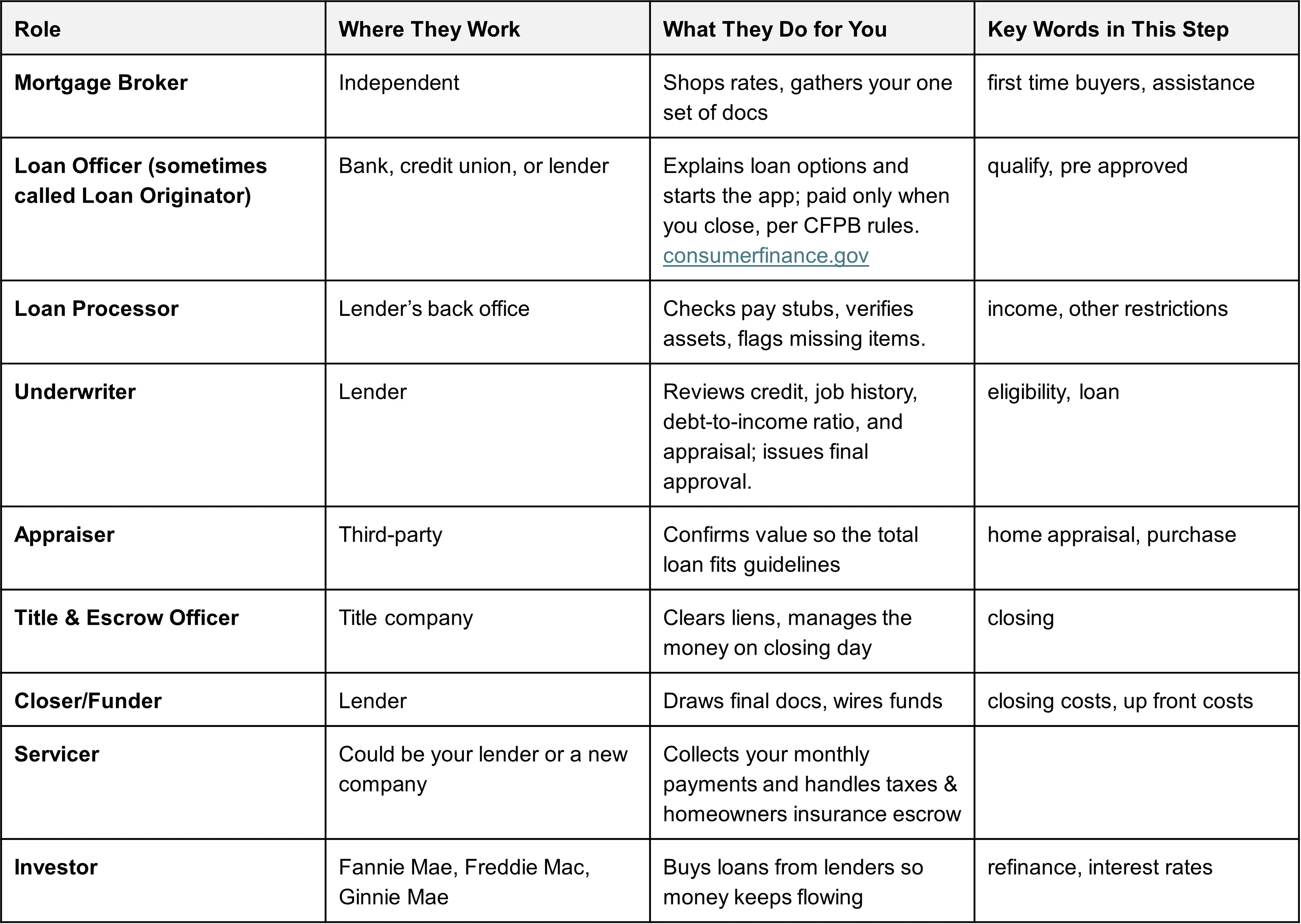

Knowing each role keeps surprises low and timelines on track.

Most first time homebuyer loans let you put down less than the old 20 percent rule:

If saving is tough, look for programs to help with your down payment that offer grants, forgivable loans, or second mortgages with no interest. Your state housing agency keeps an updated list.

Expect another 2 % – 5 % of the purchase price in closing costs—things like appraisal, title, and mortgage insurance. Many states now fund closing cost assistance programs to cut these costs for first time buyers. Ask if the seller or lender can pay part of the fees; on some loans you can roll them into the loan amount.

Because the loan is insured by the government, FHA loans accept lower credit scores (500–579 with 10 % down; 580+ with 3.5 % down) and higher debt-to-income ratios. New 2025 limits let you borrow up to $524,225 in most counties and $1,209,750 in high-cost areas. archives.hud.gov

With good enough credit (typically 680+), conventional loans can offer lower interest rates and cancelable mortgage insurance once your equity hits 20 %. New 2025 limits and higher loan types (like 2-, 3-, and 4-unit properties) broaden who can qualify.

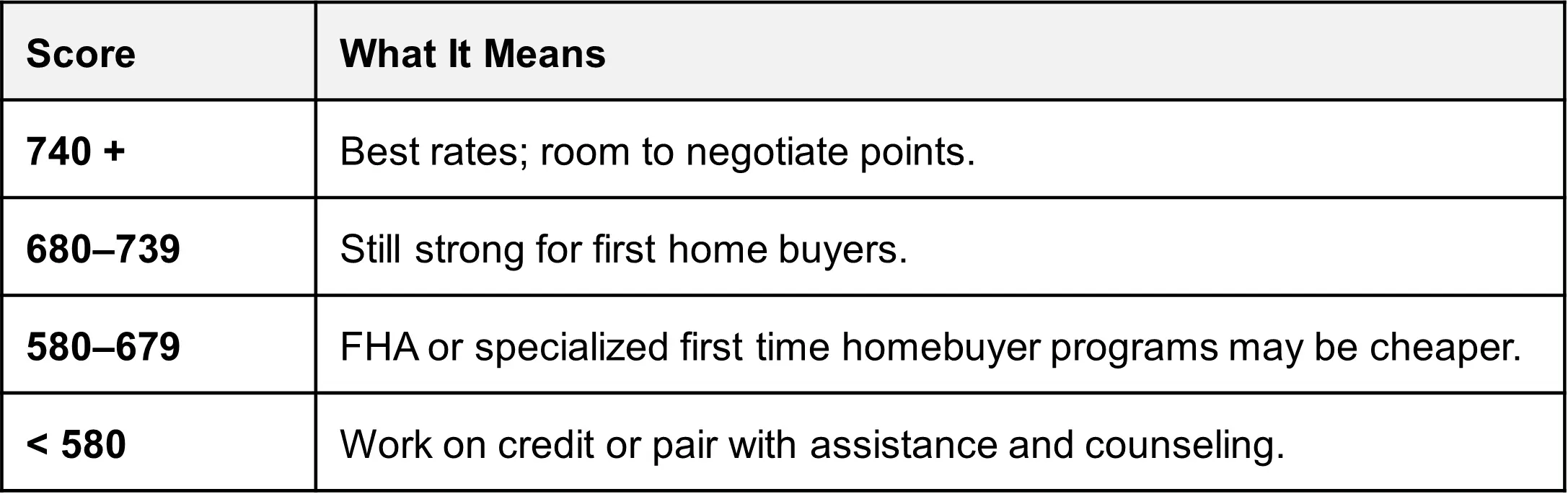

Remember, paying bills on time and keeping balances low boosts your score faster than any quick fix.

These agencies buy mortgage loans from lenders so money keeps flowing. Their 2025 rule changes increased loan limits, updated eligibility grids, and opened more refinance options for moderate-income homeowners. That means wider access and often lower interest rates for buyers who meet the income and loan amount guidelines. FannieMae.com

Visit the CFPB’s free Buying a House Roadmap for step-by-step worksheets and updated lender questions. consumerfinance.gov

If you still have questions, connect with a HUD-approved housing counselor. A quick talk can save you thousands in payment and closing costs, and put you on the smooth path to homeownership in 2025. Get started with our free, confidential counseling and education right here at Credit.org.