Buying a house is a big step. It’s exciting, but it also takes planning. If you’re a first-time homebuyer, you might feel unsure about where to start. Don’t worry—we’ll walk you through everything you need to know to get ready to buy your first home.

A down payment is the money you pay upfront when buying a house. Most lenders ask for a down payment of 3% to 20% of the home’s purchase price. If you can pay 20%, you might avoid paying for private mortgage insurance (PMI), which can lower your monthly mortgage payment.

But what if you can’t save that much? There are programs that can help. For example, the Federal Housing Administration (FHA) offers loans with lower down payment requirements. Some states and cities also have payment assistance programs to help with down payments and closing costs. Check with a local HUD-approved housing counseling agency or ask your mortgage broker for more information.

Find out more about down payments here.

Your debt-to-income ratio (DTI) is a number that shows how much of your income goes toward paying debts. Lenders use this number to decide if you can afford a mortgage loan.

To calculate your DTI:

For example, if you pay $1,200 a month on debts and earn $3,000 a month before taxes, your DTI is 40%.

Most mortgage lenders prefer a DTI below 40%. Some may accept higher, but a lower DTI can help you get better loan terms.

Your credit report shows your credit history. It includes information about your loans, credit cards, and payment history. Lenders look at your credit report to decide if you’re a good borrower.

You’re entitled to one free credit report each year from each of the three credit bureaus: Experian, Equifax, and TransUnion. You can get them at AnnualCreditReport.com.

Check your credit report for:

If you find any issues, contact the credit bureau to fix them.

Take our free online course about how to Understand Your Credit Report.

Your credit score is a number that shows how good you are at managing credit. Scores range from 300 to 850. A higher score means you’re more likely to get approved for a loan and get better interest rates.

Here’s how scores are generally viewed:

To improve your credit score:

Learn more about your credit score here.

-min.webp)

An earnest money deposit is money you put down to show you’re serious about buying a home. It’s usually 1% to 3% of the purchase price. This money is held in an account until the sale is finalized. If the deal goes through, the earnest money goes toward your down payment or closing costs.

Learn more about earnest money from the National Association of Realtors.

A home loan, or mortgage, is money you borrow to buy a house. There are different types of mortgage loans, including:

Each loan has its own requirements and benefits. Talk to a lender to find the best option for you.

Learn more about The Different Types of Home Loans.

A conventional mortgage is a loan not backed by the government. These loans often have stricter requirements:

If you can meet these requirements, a conventional loan might offer better terms and lower mortgage insurance costs.

The home buying process involves several steps:

House hunting is the fun part! Keep these tips in mind:

A home inspection is a detailed check of the home’s condition. An inspector looks at things like the roof, plumbing, electrical systems, and more.

If the inspection finds problems, you can:

Always get a home inspection before finalizing the purchase.

When home shopping, consider:

Use online listings, visit neighborhoods, and work with your real estate agent to find the right home.

Home buying is a journey. It involves saving money, understanding your finances, and making informed decisions. With the right preparation, you can find a home that fits your needs and budget.

Remember:

One of the most important parts of preparing to buy a home is figuring out what your future mortgage payment will be. This monthly cost includes more than just your loan. Here’s what goes into a typical mortgage payment:

This total is often called “PITI” (Principal, Interest, Taxes, Insurance). Make sure you can comfortably afford this amount based on your monthly gross income. Many experts suggest that your mortgage should be no more than 28% to 30% of your gross monthly income.

Getting pre-approved shows sellers that you’re a serious buyer. A pre-approval letter from your lender states how much you can borrow based on your financial situation.

To get pre-approved, you’ll need:

Once you’re ready to buy, you’ll submit a full mortgage application. This includes more documents and sometimes additional information. Be ready to respond quickly to your lender so the process moves smoothly.

Saving is a huge part of how to prepare to buy a house. While your down payment is the biggest chunk, there are other upfront costs to consider, including:

It’s smart to start saving as early as possible. Even small amounts each month can add up. Automate your savings to make it easier. You may also qualify for payment assistance programs that help with upfront costs.

Don’t settle for the first lender you talk to. Comparing offers from multiple lenders can help you find the best financing. Look for differences in:

Different lenders may offer you different mortgage options based on your credit score, income, or type of home. Use a mortgage calculator to compare your choices and estimate your monthly payment.

Before you start house hunting, you need to know how much house you can afford. This depends on:

Use online tools or ask a lender to help estimate your budget. Remember that just because you qualify for a large loan doesn’t mean you should take it. Stick to a price range that allows you to save money and avoid stress.

When choosing a mortgage, pay attention to:

A lower interest rate means a lower monthly payment. But shorter loan terms may have higher monthly payments with lower total interest paid over time. Longer terms often cost more in the long run but ome with smaller monthly bills.

Ask your lender for side-by-side comparisons of different options.

Before you buy a home, it helps to strengthen your finances. Here’s how to improve your financial situation and borrowing power:

A higher score can help you qualify for a lower interest rate, which saves you thousands over the life of your loan.

Many first time homebuyers make avoidable mistakes. Here are some to avoid:

Planning ahead helps you avoid setbacks later in the home buying process.

Read more about 10 First Time Home Buyer Mistakes to Avoid.

Once you’ve applied for a home loan, avoid doing anything that might lower your credit score:

Lenders will likely check your credit again before closing. Keep your credit history steady to avoid delays or changes to your mortgage loan offer.

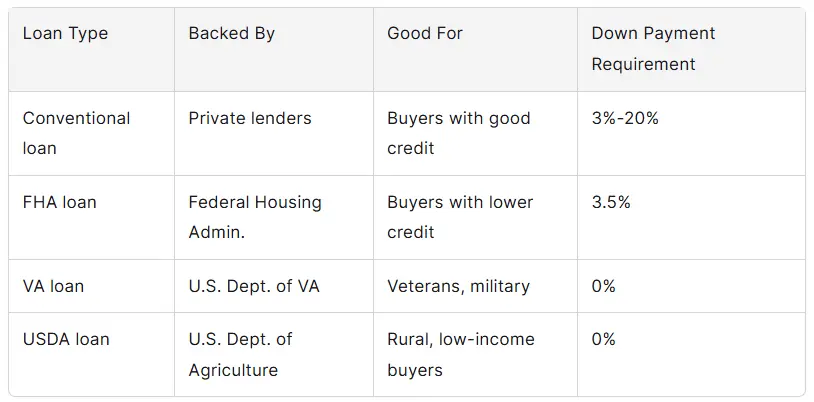

There are many mortgage options available. Here’s a quick comparison:

Each loan has different benefits, and the right one for you depends on your financial situation and long-term goals.

Markets change fast. Mortgage rates may go up or down. Property taxes can increase. Your income or debt might change. That’s why it’s smart to re-evaluate your homebuying plan regularly.

Keep asking yourself:

Stay flexible and check in with your real estate agent or lender as your situation evolves.

By now, you’ve learned how to prepare financially and what lenders are looking for. Let’s walk through the final steps in the home buying process in more detail so you can feel confident about what’s ahead.

A great real estate agent is key to a successful home purchase. Your agent will:

Look for an agent who works with first time homebuyers, understands your local housing market, and communicates well.

House hunting is more than just looking at pretty houses online. It’s about matching your budget with your needs and long-term goals.

Keep these tips in mind:

If you’re serious, you’ll likely need to submit an offer quickly once you find the right home. That’s where your earnest money deposit and pre-approval letter come in handy—they show you’re ready to move forward.

Once you’ve found your dream home, your agent will help you put in an offer. This includes:

The seller might accept, reject, or come back with a counteroffer. Your agent will help you through negotiations until both sides agree.

A home inspection is one of the most important steps for first time buyers. A licensed inspector will check:

The goal is to uncover any issues before you finalize the purchase. If there are serious problems, you can:

Never skip a home inspection, even if the house looks perfect. It’s your safety net.

The appraisal is done by a third-party professional who determines how much the house is worth. Your lender needs this to make sure the home is worth what you’re paying.

If the home appraises for less than your offer:

Appraisals protect both you and your mortgage lender from overpaying.

At this stage, your mortgage application moves into underwriting. This is when the lender verifies everything—your income, job, savings, debts, and credit.

Avoid changing jobs, taking on new auto loans, or making large purchases while your loan is being approved.

You’ll need to submit more documents if requested, like updated paycheck stubs, bank statements, or letters of explanation for anything unusual in your credit history.

Once underwriting is complete, your loan will be approved and scheduled for closing.

A few days before closing, you’ll receive a closing disclosure. This outlines your:

Review everything carefully. Compare it to your original loan paperwork. Ask your lender or real estate agent to explain anything you don’t understand.

On closing day, you’ll meet at a title company or attorney’s office to sign your documents. You’ll bring:

Once you sign all the paperwork and the deal is recorded with the local government, you’ll get the keys to your new home. Congratulations—you’re now a homeowner!

Buying the home is just the beginning. Here’s what you should do next:

Being a homeowner also means learning about local rules, such as HOA requirements, trash pickup days, and how to file for a homestead exemption if your state offers it.

As a homebuyer, especially as a first time buyer, you have rights under the law. These include:

If you ever feel unsure or pressured, speak with a HUD-approved housing counselor for guidance.

Eventually, you may want to refinance your home to:

Refinancing requires a new credit check, income documentation, and an updated appraisal. Keep your credit score high and your debt-to-income ratio low to qualify for better terms.

Homeownership is a huge milestone. It means stability, equity, and a place to call your own. Now that you’ve followed each step of the home buying process, you’re ready to enjoy the results of your hard work and smart planning.

Remember to continue managing your:

When you’re learning how to prepare to buy a house, the right tools can make a big difference. Here are some that help you make informed decisions:

Use a mortgage calculator to estimate:

These tools can also show how different down payment amounts affect your loan balance and whether you’ll need to pay private mortgage insurance.

These help determine how much house you can afford based on your:

Some calculators even factor in auto loans, student debt, and credit card balances to better estimate your debt-to-income ratio.

If you’re a first time homebuyer, you might qualify for homebuyer education and payment assistance programs. These programs are offered by:

These classes can teach you:

Completing a homebuyer education class may also qualify you for down payment help or a better mortgage rate from some lenders.

Many state and city programs offer payment programs for first time buyers, including:

Check your state housing agency or HUD’s resource map to explore what’s available in your area. Most programs have income limits and require the home to be your primary residence.

Before choosing a lender or loan type, ask:

Good lenders will explain each part of the process in simple terms and help you feel confident.

There’s a lot of paperwork involved in the mortgage application. Be ready to supply:

This helps your lender verify your ability to afford your future mortgage payment and approve your home loan.

The housing market changes constantly. High demand can drive up prices, while higher mortgage rates can reduce how much house you can afford. In 2025, many markets remain competitive, especially for entry-level homes.

Be prepared to:

Your real estate agent can guide you based on up-to-date housing market conditions in your area.

Once you close on your new home, it’s important to continue managing your credit wisely:

This will help protect your credit score for future refinancing, home improvements, or new financial goals.

Here are a few terms first time buyers should know:

Buying your first home is one of life’s biggest milestones. It’s about more than finding a house—it’s about financial readiness, smart planning, and making informed decisions every step of the way.

Let’s review a few final reminders:

With the right team, the right mindset, and solid preparation, you’ll not only become a homeowner—you’ll stay financially stable for the long haul.

Buying a home is a big step, but with the right guidance, you can make it a successful one.

Remember, Credit.org offers free housing counseling and credit counseling is available on demand. Take advantage of the free resources available to you to be as prepared as possible to spring into homeownership.