Buy Now, Pay Later (BNPL) lets you split a purchase into smaller payments instead of paying the full price upfront. In most cases, you take the item home immediately and repay the balance over a few weeks or months. These plans have become especially common for online purchases like clothing, electronics, and other items that might not comfortably fit into a single month’s budget.

As BNPL has become more common, so has confusion about what it actually costs and how it fits into a broader financial picture. Used carefully, it can smooth cash flow for a short period. Used carelessly, it can create new payment obligations that are easy to underestimate.

What began as a niche checkout option is now part of a broader shift in consumer credit. BNPL is no longer limited to a handful of fintech apps. Major credit card issuers, large retailers, and traditional financial institutions now offer their own versions.

According to a report from Morgan Stanley, BNPL usage is expected to continue growing, particularly among younger consumers. Faster approvals, short repayment windows, and the promise of no interest have made these plans appealing.

At the same time, this style of borrowing raises practical questions. BNPL doesn’t always behave like a credit card or a traditional loan, and the long-term effects on budgeting, cash flow, and credit are not always obvious at the point of purchase.

Choosing BNPL at checkout means agreeing to a short-term loan. The BNPL provider pays the retailer in full, and you repay the provider according to a fixed schedule. Payments are usually due every two weeks or once a month, depending on the plan.

A typical BNPL transaction looks like this:

Most BNPL plans do not involve a traditional loan application, and many providers avoid hard credit checks. That convenience and soft credit check is part of the appeal, but it also means fewer friction points before taking on debt.

BNPL loans differ from traditional loans in several important ways. They tend to be smaller, shorter in duration, and are often marketed as interest free at the outset. That does not make them risk free.

Late fees, processing fees, deferred interest, and overlapping payment schedules can quickly change the cost of a BNPL purchase, especially when multiple plans are active at the same time.

BNPL plans often come with late fees, and some may start to charge interest if you miss a payment or don’t finish your plan on time. This can make what seemed like a low-cost option much more expensive.

Many BNPL loans are structured to have predictable monthly payments. For example, a $200 purchase might be split into four $50 payments due every two weeks. If a monthly plan is offered, the amount might be spread across three or six months instead.

Make sure to review the payment schedule closely. Automatic payments help avoid missed payments, but they also require careful tracking of your bank balance. If your account has insufficient funds, you could be hit with overdraft charges or late fees.

Most BNPL services advertise interest free installment options. In these cases, you won’t pay more than the purchase amount if you follow the terms. This can be a helpful way to break up a major purchase while paying zero interest.

However, some providers offer “promotional” interest free payments. If you don’t pay off the balance by a set date, you may be charged interest retroactively. Always read the terms carefully and look for language about “deferred interest.”

Not all BNPL plans are interest free. Some offer longer repayment periods—like six to twelve months—but begin to charge interest once the promotional period ends. This interest can be higher than what you’d pay on a credit card.

Before you agree to a plan, check whether the provider will charge interest and under what conditions. Some may have high annual percentage rates (APRs), especially for users who miss a payment.

In the past, most BNPL lenders didn’t report payment activity to credit bureaus. But this is starting to change.

If your BNPL provider reports to the major credit bureaus, your payment history can help build or hurt your credit score. Timely payments may improve your credit history, but missed or late payments can bring your score down.

This matters most if you’re building or rebuilding credit. A single missed payment can have a lasting impact on a customer's credit score.

When BNPL activity is reported, it may include:

Most BNPL providers only report to one or two of the three main credit bureaus. Some do not report at all. Be sure to ask whether the BNPL loan will be included in your credit file.

BNPL services are not free passes. If you miss a payment, you may face:

The Consumer Financial Protection Bureau warns that late payments and missed BNPL obligations can create a snowball effect. If you can’t make your payments, it may be better to cancel or return the item than fall into debt.

BNPL services are often delivered through apps like:

These apps work with retail partners, both online and in stores. You may also see them offered directly at the checkout screen on retail websites.

Some apps offer physical or virtual cards that can be used like a debit or credit card, spreading purchases over time automatically.

-min.webp)

Many shoppers choose to pay monthly for better budgeting. Breaking a large expense into smaller monthly payments can make the cost feel more manageable.

People may also choose monthly plans because:

While this may work for some, it’s important to make sure your total monthly debt payments don’t exceed what you can afford. Just because a monthly plan is offered doesn’t mean it’s the best financial choice.

Both BNPL plans and credit cards allow you to spread payments over time, but they operate very differently once you look past the checkout screen.

The BNPL payment option typically skips a full credit application and locks you into a fixed repayment schedule. Credit cards require underwriting, but give you more control over how and when balances are paid down. Interest works differently as well. BNPL may offer short interest-free windows, while credit cards generally accrue interest unless balances are paid in full.

Credit reporting also differs. Credit card activity is reported consistently across all bureaus. BNPL reporting depends on the provider and may only appear if something goes wrong. That difference matters if credit building or protection is part of your plan.

For some purchases, either option can work. Credit cards, however, usually come with stronger protections, including dispute rights, fraud coverage, and warranty benefits that BNPL users don't get.

BNPL is increasingly used for larger purchases like electronics, furniture, and appliances, often spread across six or twelve payments instead of the standard four.

Before using BNPL for a larger expense, it helps to slow down and pressure-test the decision:

BNPL can work for a one-time purchase with a clear payoff path. It becomes riskier when it turns into a default way to handle big expenses.

Some BNPL plans delay the first payment by 30 days or more. These are often marketed as “later loans” and are designed to give temporary breathing room.

That delay can help in the short term, but it shifts risk forward. Some plans begin charging interest after the delay period, while others shorten the remaining repayment window. The cost depends entirely on the terms, not the marketing label.

Before choosing a delayed plan, confirm when payments actually start and what happens if the balance isn’t cleared on time.

BNPL providers often emphasize convenience and speed, but the experience can change once a problem arises.

Common issues reported by users include slow responses to disputes, unclear refund timelines, and difficulty reaching support when payments fail or returns are involved. When something goes wrong, BNPL plans may not offer the same dispute protections as credit cards.

Researching support policies before using BNPL matters more than the checkout experience itself.

Repayment terms vary widely across BNPL providers. Some plans involve four equal payments over six weeks. Others extend payments across several months.

Before agreeing to a plan, it’s worth confirming:

Clear terms make the difference between a manageable plan and an expensive surprise.

Many BNPL plans are structured around four payments for a practical reason, not convenience. This is so common that these payment plans are often called "pay in four loans".

Under federal law, loans requiring more than four installments typically fall under the Truth in Lending Act (TILA). That brings additional disclosure requirements and consumer protections. By limiting plans to four payments or fewer, some BNPL providers avoid those obligations.

This structure helps keep costs down for providers, but it also means consumers may receive fewer disclosures and protections than they would with traditional credit products. Reading the fine print matters more, not less, in these cases.

Despite “no interest” messaging, BNPL plans can still generate costs. Fees may apply when payments are missed, withdrawals fail, or accounts require ongoing servicing.

Common charges include late fees, returned payment fees, and service fees tied to account activity. When multiple plans are active, tracking these costs becomes harder and mistakes become more expensive.

Multiple BNPL plans create overlapping payment schedules. This often happens during sales periods or holidays, when small purchases add up quickly.

Four separate $100 purchases can easily translate into multiple withdrawals every two weeks. Without careful tracking, it becomes easy to misjudge cash flow and miss payments.

Outstanding loans aren’t inherently dangerous, but they demand more attention than many users expect.

Loan stacking occurs when several BNPL plans are active at the same time without a clear payoff strategy.

Because approvals are fast and friction is low, stacking can happen before the financial impact is fully felt. Missed payments, growing fees, and credit complications often follow.

Treating each BNPL plan like a traditional loan helps reduce this risk. If the payment schedule can’t fit comfortably into your budget, the purchase likely needs to wait.

BNPL’s effect on credit depends on reporting practices, which are inconsistent across providers.

Some companies report all activity. Others report only missed payments or defaults. That means a plan could damage credit without offering any upside when payments are made on time.

This unpredictability makes BNPL different from credit cards, installment loans or personal loans, where reporting rules are clearer.

BNPL activity can influence credit through payment history, total debt, and credit utilization, depending on how it’s reported.

Missed payments can lower scores. Unreported activity won’t help build credit. If BNPL balances are treated as revolving credit, utilization ratios may increase.

As credit scoring models evolve, BNPL’s role is expanding, but it remains uneven across bureaus.

Some BNPL providers now share limited data with credit bureaus, including payment history and open plan counts. Others report only under specific conditions.

If credit building is a goal, understanding a provider’s reporting policy is just as important as understanding its payment terms.

Flexible payment structures are part of BNPL’s appeal. Options may include biweekly or monthly schedules and varying term lengths.

Flexibility helps when cash flow is predictable. It becomes a liability when smaller payments mask the total cost. Choosing the shortest affordable term reduces risk and keeps repayment manageable.

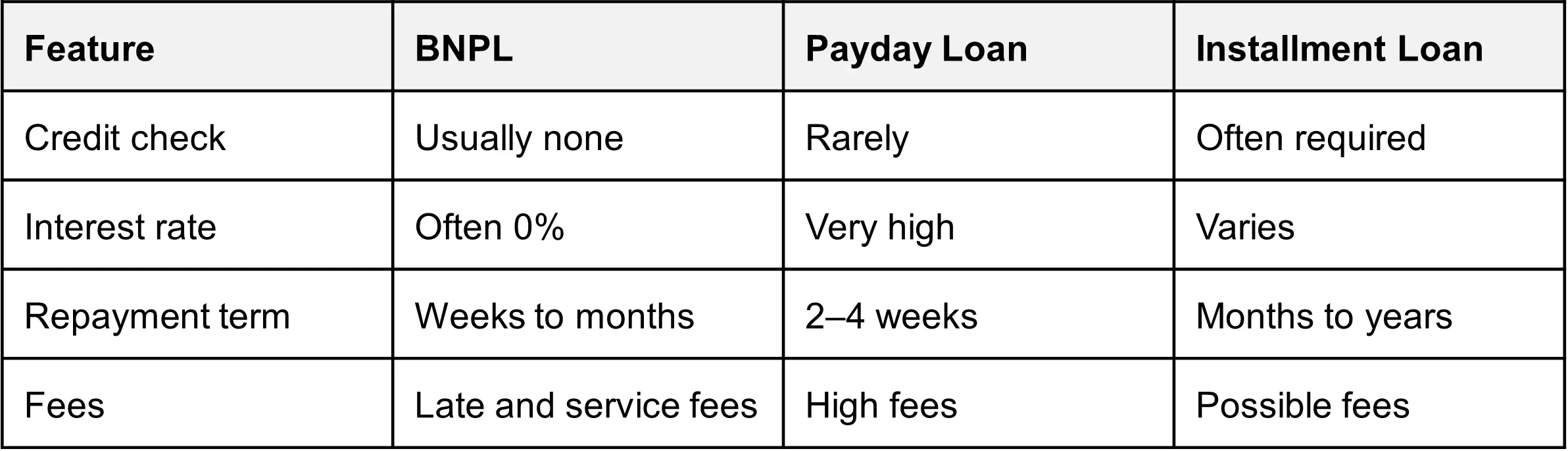

Buy now, pay later plans are often described as an alternative to short-term loans, but the comparison only goes so far. While BNPL is usually cheaper than payday lending, it still relies on short repayment windows and automatic withdrawals, which can strain cash flow if timing is off.

Here’s how BNPL typically compares to other short-term borrowing options:

BNPL avoids the extreme costs of payday loans, but it still creates repayment obligations that can pile up quickly if multiple plans overlap or income changes unexpectedly.

The Consumer Financial Protection Bureau has been paying closer attention to the buy now, pay later industry as these products become more common.

Regulators have raised concerns about:

The CFPB has been clear on one point: even when marketed as a convenience feature, BNPL is still a form of debt. Consumers need clear information and fair safeguards, especially as these plans become part of everyday spending.

BNPL plans don’t always provide the same dispute protections as credit cards. If a product never arrives, is returned, or is defective, resolving the issue can take longer and involve more back-and-forth than consumers expect.

Some providers offer in-app dispute tools, but those systems vary widely in effectiveness. In certain cases, payments continue while a dispute is being reviewed, leaving consumers paying for items they no longer have.

Before using BNPL (especially for online shopping), it helps to confirm whether the provider:

If those protections aren’t clearly stated, a more traditional payment method may offer better recourse.

One reason BNPL has spread so quickly is how little friction exists at signup. The process is designed to feel closer to a checkout step than a loan application.

In most cases:

Hard credit checks are uncommon, though some providers may run soft checks to set limits or flag risk. That ease of approval is appealing, but it also means fewer guardrails before taking on repayment obligations.

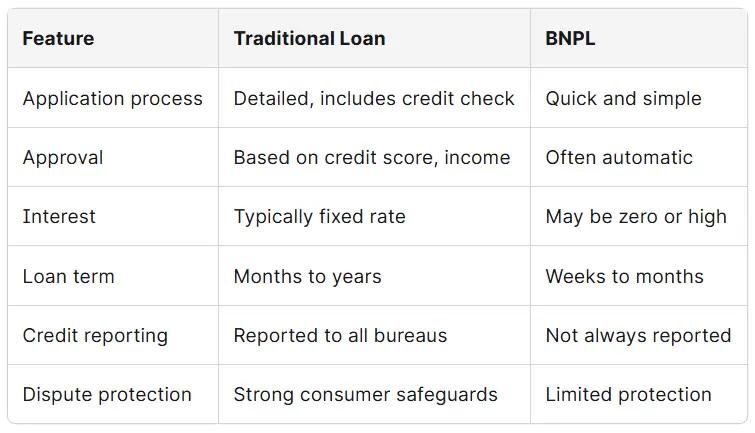

BNPL and traditional loans serve different purposes, even though both involve paying over time. Traditional loans take longer to arrange, but they offer clearer terms and stronger consumer protections.

Here’s a general comparison:

Traditional loans require more upfront effort, but they’re often easier to manage over time, especially for larger amounts or longer repayment periods.

Buy now pay later users come from all age groups, but usage is especially high among Gen Z and Millennials. Many users cite the following reasons for choosing BNPL:

But research from Consumer Reports and Morgan Stanley has found that many BNPL borrowers don’t fully understand how buy now pay later plans work, or how they affect their long-term finances.

While many BNPL plans are advertised as free, the reality is more complex. Even if you avoid interest, you may still face other costs, including:

Also, many providers allow you to “refinance” or defer your payments for a fee. This can create a cycle of revolving debt that’s hard to escape.

Aside from the obvious fees, some BNPL apps charge:

Always check the provider’s full terms before signing up. If something sounds too good to be true, it probably comes with hidden costs.

The real risk with buy now, pay later isn’t any single purchase. It’s what happens when several small commitments overlap. Because approvals are quick and payments are automated, it’s easy to lose sight of how much money is already spoken for.

That usually shows up in predictable ways. Due dates blur together. Withdrawals hit your account before you’ve adjusted your spending. Fees start appearing not because the purchase was unreasonable, but because the timing didn’t line up.

A handful of $25 weekly payments can quietly turn into a triple-digit drain on cash flow, before essentials like groceries, utilities, or rent even enter the picture.

Most BNPL providers require automatic payments, and the method you choose determines how much room for error you have.

Debit cards are simple, but they leave no buffer if your balance runs low. Bank accounts offer more flexibility, but only if you’re actively tracking deposits and withdrawals. Some services allow credit cards, which can create a different problem, using one form of debt to cover another.

The safest option is the one that gives you visibility and control. If you can’t easily see when money is leaving your account, you’re more likely to get surprised by fees.

BNPL plans don’t always advertise a traditional credit limit, but limits exist. Providers adjust how much you can spend based on how often you use the service, whether you pay on time, and how your account behaves over time.

That flexibility cuts both ways. Responsible use may increase available spending. A single missed payment can freeze or reduce access without warning.

Because limits shift quietly, it’s easy to assume you have more room than you actually do, right up until a transaction is declined or an account is locked.

Payment flow is simply the rhythm of money moving in and out of your account. With BNPL, that rhythm is set by the provider, not you.

Automatic withdrawals mean you need to know exact dates, processing times, and how refunds are handled if something goes wrong. When a return takes longer than expected, payments may continue even though the item is already gone.

If you’re not actively tracking each plan, small timing issues can snowball into overdrafts or returned payments that cost more than the original purchase.

BNPL apps are designed to encourage repeat use. Notifications, special offers, and “pre-approved” messages all lower the friction for making another purchase.

That’s fine if the first plan is already paid off. It becomes a problem when new transactions stack on top of existing ones.

Turning off notifications, keeping purchases intentional, and limiting BNPL to planned expenses helps prevent the slow drift from convenience into dependency.

If buy now, pay later is becoming a regular tool rather than an occasional one, it’s worth stepping back and looking at alternatives.

Setting aside small amounts ahead of time for known expenses removes the pressure to borrow. Layaway programs, where available, slow the process down and eliminate repayment risk. A written budget can expose patterns that BNPL hides by breaking costs into pieces.

None of these options are exciting, but they reduce the need to make decisions under time pressure.

Credit.org provides tools and education designed to help people make decisions before debt becomes the default solution. Whether you’re dealing with credit card balances, uneven monthly expenses, or recovering from a difficult financial stretch, understanding your options matters.

You can explore practical guidance on topics like:

Reducing reliance on short-term borrowing starts with clearer information and fewer reactive decisions.

Buy now, pay later isn’t inherently good or bad. Like any borrowing tool, outcomes depend on how it’s used. Used occasionally, with a clear payoff path, it can smooth timing issues. Used frequently, or without tracking, it can quietly strain cash flow and increase financial stress.

Before committing to a plan, it’s worth asking whether the payments fit comfortably into what you already owe, not just whether they look manageable on their own.

The goal isn’t to avoid every form of credit. It’s to avoid surprises.

If BNPL plans, credit cards, or uneven expenses are starting to feel difficult to manage, you don’t have to sort it out alone. A full review of your situation can surface options that aren’t obvious at checkout.

Credit.org offers:

A conversation with a certified counselor can help you decide what fits your situation now, not what an app assumes will work.