Paying off debt can feel overwhelming, especially when you have multiple balances with different interest rates, minimum payments, and due dates. Knowing where to start is one of the most important steps in your debt repayment journey. Should you tackle the smallest balance first or go after the debt with the highest interest rate?

Two popular strategies can help: the debt snowball method and the debt avalanche method. Each approach has its benefits, and choosing the right one depends on your financial situation, personality, and long-term goals.

In this guide, we’ll break down each method, explain how they work, and help you decide which one may be right for you.

Before you choose a repayment method, you need a clear picture of your total debt. Start by listing all of your balances, including:

Note each account’s interest rate, monthly payment, and total amount owed. Be honest about your current financial situation, including how much extra money you can put toward debt repayment each month.

This overview helps you determine whether you’re dealing with mostly high-interest revolving accounts like credit cards, or a mix that includes installment loans with fixed interest rates.

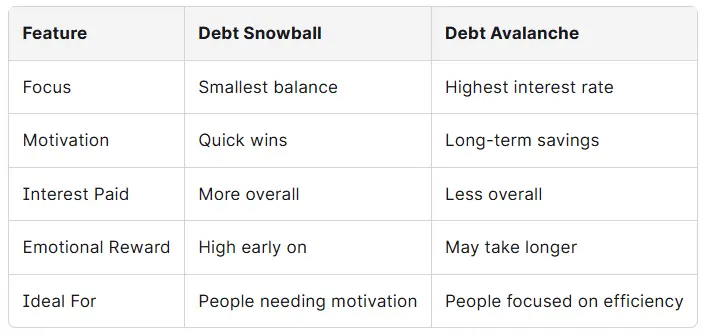

The debt snowball method focuses on paying off your smallest debt first while continuing to make minimum payments on all other debts. Once the smallest is gone, you move to the next smallest, and so on. With each debt you eliminate, you gain momentum, just like a snowball rolling downhill.

This method gives you quick wins, which can be incredibly motivating. It helps you build confidence and create a sense of progress, even if you’re not saving the most on interest payments right away.

Let’s say you have the following debts:

With the snowball method, you would pay off the $500 credit card first, even though it has a lower total cost than the other debts. The goal is to eliminate accounts quickly, reduce the number of bills, and stay motivated.

The debt avalanche method takes a different approach: instead of focusing on balance size, it targets the highest interest rate debt first. This strategy saves more money in the long run by reducing how much interest you pay.

Using the same debts from above, the avalanche method would have you pay off the $500 credit card at 18% first, followed by the $2,000 personal loan at 10%, and then the auto loan at 6%.

While you may not pay off your first debt as quickly as with the snowball method, you’ll likely save more money over time by reducing interest rates sooner.

Let’s look at the main differences between the two strategies:

There’s no one-size-fits-all answer. If you’ve struggled to stay committed to a debt repayment strategy, the snowball method may keep you going. If your priority is minimizing the total cost of debt, the avalanche method is the better financial move.

Both methods can positively impact your credit score over time. As you pay down balances and lower your credit utilization ratio, your score will likely improve. However, be careful not to close paid-off credit cards too soon; keeping them open can help maintain a healthy credit utilization percentage, as long as there’s no annual fee.

If you’re dealing with high-interest credit card debt, a balance transfer credit card might help. These cards often offer 0% interest for an introductory period, usually between 6 to 21 months. That gives you a window to pay off your balance without accruing more interest.

However, balance transfers are not risk-free. Watch out for:

Also, to qualify, you’ll typically need a good to excellent credit score. If your credit needs improvement, this option may not be available right away.

Another option is debt consolidation, which combines multiple debts into one monthly payment. This can help simplify your finances and potentially reduce your interest rate. You can consolidate through:

While the idea of one debt sounds appealing, it’s crucial to understand the real costs involved. Be wary of companies that promise easy fixes or advertise debt consolidation loans with hidden fees or high interest rates.

Instead, look for a trusted nonprofit agency that offers a debt repayment plan without requiring new loans. Credit.org's debt management program is one such option, helping you pay down balances with lower interest and no new borrowing.

-min.webp)

When deciding which debt to pay down first, consider these questions:

Use your answers to guide your decision. If you’re dealing with high interest but can afford to stay focused, the avalanche method may work best. If your biggest challenge is staying consistent, the snowball method may help you build and maintain momentum.

Medical debt is a growing burden for many Americans. According to a recent WMUR report, 1 in 4 people struggle with unpaid healthcare bills. This type of debt usually doesn’t carry interest but can still hurt your credit if left unpaid.

Consider using the snowball method if your medical bills are small and scattered. If you’ve negotiated a single large payment plan, the avalanche method could reduce your overall stress if other debts have high interest attached.

The debt avalanche is especially useful when dealing with high interest credit cards. These revolving debts often carry rates of 20% or more. Paying them off first will significantly reduce your total repayment costs.

If you’re unsure which cards have the highest interest rate, check your billing statements or contact your card issuers. You might also consider using a credit report review service to organize your accounts and spot problem areas.

It’s possible to focus on prioritizing debt without giving up on saving. While you should concentrate on paying off high-interest balances, set aside a small emergency fund to avoid falling back into debt due to unexpected expenses.

Try splitting your extra funds: most can go to debt, but reserve a small portion for savings. Even $25 a month can build a helpful cushion.

Only making minimum payments might keep you current, but it’s a long, expensive road. On a $5,000 credit card with a 20% interest rate, paying the minimum could take decades and cost thousands in interest.

This is why creating a clear debt repayment plan is essential. Whether you use the snowball or avalanche, the key is to pay more than the minimum whenever possible.

Maintaining a healthy credit score during repayment is possible. Here’s how:

Your goal isn’t just to pay off debt; it’s to create a solid foundation for long-term financial wellness.

Sometimes it’s tempting to pay off a big debt because the size of the balance feels stressful. But that may not be the most cost-effective move. Unless that large debt carries a high interest rate, you might be better off focusing on smaller or higher-interest balances first.

However, if that big debt is interfering with your credit, relationships, or quality of life—like a delinquent student loan or a car loan near repossession—prioritize it for peace of mind.

Absolutely. Many people find success by creating a hybrid debt repayment strategy. For example:

This blended approach allows for motivation and savings at the same time. The key is consistency and commitment to your overall goal of becoming completely debt free.

There’s a lot of questionable advice out there about which debt to pay down first. Some people suggest using a home equity loan or 401(k) withdrawal, but these options can be risky and could leave you worse off long term.

Avoid advice that:

Stick to trusted sources like ConsumerFinance.gov or USA.gov for unbiased, government-backed guidance.

Use budgeting apps, spreadsheets, or printable tools to monitor your progress. A few tips:

If you prefer a more visual approach, try a debt payoff tracker or thermometer-style chart.

If you’re unsure whether the debt avalanche method or snowball method is right for you, you don’t have to figure it out alone.

Nonprofit credit counselors can walk you through your options and help build a personalized debt repayment plan. They’ll review your entire debt situation, explain how different strategies affect your credit score, and help you avoid scams.

We've done the math on comparing the debt snowball method to the debt avalanche method, so give us a call if you need help making the right choice between debt payoff methods.

Whether you choose to focus on the highest interest debt or the smallest debt, the most important step is starting. Consistent effort will get you closer to financial freedom.

If you’re ready to take the next step, Credit.org can help. Our certified nonprofit counselors offer free credit counseling, personalized debt repayment strategies, and trusted advice tailored to your needs. We don’t recommend taking out new loans, we help you work with what you have.

Explore our services:

Take the first step toward becoming debt-free. Talk to a counselor today and start building your path to financial wellness.