When you hit financial hardship, your lender may offer a temporary break from your mortgage payments. That relief usually comes as either deferment or forbearance. Both can pause or reduce what you owe for a time, but the mechanics are not the same, and the long-term impact can differ. Knowing how each one works can make a real difference in protecting your home and your broader financial footing.

This guide walks through how deferment and forbearance function in practice, what circumstances typically qualify, and how to weigh your options. It also clarifies terms such as payment pause, interest accrual, and repayment options, so you understand exactly what you are agreeing to before you move forward.

Your monthly loan payments usually cover more than just the loan principal. Each payment often includes interest, property taxes, and insurance. Missing a few payments can lead to serious consequences, like late fees or foreclosure. If you’re struggling, the worst thing to do is ignore the problem. Talk to your loan servicer immediately to explore your options.

Even a short break from your loan payments, if done the right way, can keep your credit intact and help you avoid long-term damage. But not all relief options work the same way. That’s where deferment and forbearance come in.

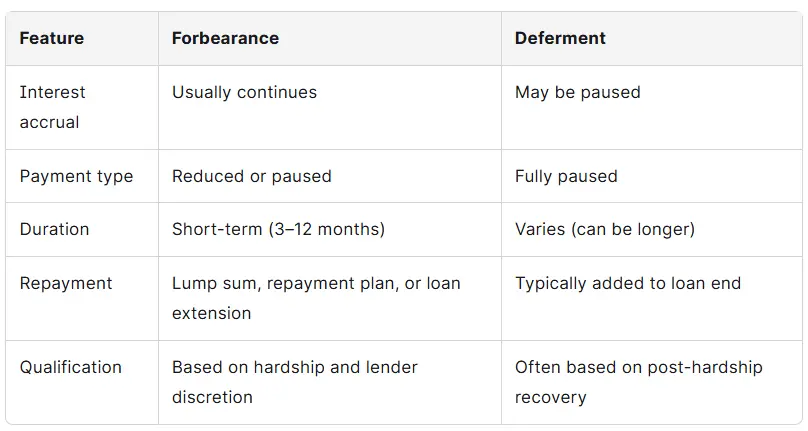

Loan forbearance allows you to temporarily reduce or stop making payments. This option is usually granted by your lender when you’re facing a short-term hardship like job loss, medical bills, or natural disaster recovery. Unlike deferment, forbearance doesn’t usually stop interest from building up during the pause. That means your loan balance can grow.

Most forbearance plans are short-term; usually three to six months. However, extensions are possible depending on your lender’s policies and your financial situation. Always get the terms in writing and confirm how interest accrues during the forbearance period.

Mortgage forbearance became a household term during the COVID-19 pandemic, when millions of homeowners were granted a temporary pause on their payments. While those programs were federally mandated, today’s forbearance programs are typically offered at the lender’s discretion.

To qualify, you’ll usually need to outline your financial situation and document the hardship. Common reasons include:

Some lenders provide general forbearance at their discretion, while others limit approval to mandatory forbearance tied to specific events. Before agreeing to anything, confirm whether interest will accrue during the payment pause and how repayment will be handled once regular payments resume.

Loan deferment also postpones payments, but the structure is not identical. In certain deferment arrangements, interest does not accrue during the pause, particularly when the loan is federally backed or connected to disaster relief. That said, it is not automatic, and private mortgage lenders may handle interest differently.

Deferment is often finalized after the immediate hardship has passed. A homeowner who lost a job, for instance, might complete a trial repayment period and then have the remaining missed payments deferred. Those skipped amounts are commonly added to the end of the loan term rather than repaid right away.

Both provide short-term breathing room, but the details matter. Key differences include:

Choosing between the two comes down to your lender’s guidelines, the nature of your financial hardship, and what you can realistically handle once payments restart.

A payment pause may be available if you are dealing with financial hardship tied to situations such as:

Your loan servicer will review your financial situation and decide whether deferment, forbearance, or another repayment plan makes the most sense. Reaching out early matters; waiting too long can limit your options.

Learn more about housing counseling services offered by Credit.org, which can help you sort through these choices and prepare for the conversation with your servicer.

Neither deferment nor forbearance lasts forever. When the pause ends, regular monthly payments resume, and the skipped amounts must be addressed. How that happens depends on the type of assistance and your lender’s policies.

Under a forbearance plan, repayment may take one of several forms:

With deferment, the missed payments are often moved to the end of the loan term, extending how long you pay but avoiding an immediate catch-up period. Even so, the exact treatment varies, and eligibility for full deferment is not guaranteed.

When you are experiencing financial hardship, contact your loan servicer right away. The servicer manages your monthly payments and oversees the application process for temporary relief, even if a different company originally funded the loan. Ask clearly:

Lenders typically require proof of economic hardship or financial difficulties, such as layoff notices, medical bills, disaster declarations, or evidence of reduced monthly income. In some cases, a qualifying event, like active duty service, National Guard activation, or another defined circumstance, may trigger mandatory forbearance. In other situations, approval will vary depending on your servicer’s internal policies.

See Credit.org’s advice on writing a hardship letter to your lender.

Once the payment pause ends, several paths may be on the table:

If the details are unclear, request a written explanation of every available repayment plan. Pay close attention to how interest accrued during the pause and whether it was added to your principal balance.

Different hardships call for different tools. You may lean toward:

If you are weighing these options, a nonprofit housing counselor or financial coach can help review your numbers and walk through the longer-term consequences before you decide.

Most articles on this topic focus on student loans, but mortgage loans follow a different set of rules. Many servicers offer mortgage forbearance after qualifying hardships like:

Mortgage deferment is less common but may be available through government programs or specific lenders. Always clarify which program you’re being offered.

This HUD.gov guide to avoiding foreclosure provides trustworthy, up-to-date information on mortgage relief programs.

If managed properly, deferment and forbearance should not hurt your credit. Most lenders will not report paused payments as delinquent if the relief was approved ahead of time. However, interest may continue to accrue, increasing your loan balance.

Late or missed payments that are not part of an approved pause can hurt your credit score. Do not stop paying until you have written confirmation that forbearance or deferment has been granted and properly documented.

If you are unsure how your servicer reported the account, review your credit report. You can request a free copy at AnnualCreditReport.com each week.

A few missteps can make a difficult situation worse:

Loan deferment, mortgage forbearance, and any payment pause can create real strain. You do not have to sort it out alone.

Credit.org’s housing counselors offer one-on-one guidance for homeowners facing hardship. They can help you understand the application steps, review your options, and map out a realistic plan going forward.

You can also look into established government resources such as ConsumerFinance.gov or DisasterAssistance.gov for additional information.

Although this article focuses on mortgage loans, it helps to see how deferment and forbearance work for student loans, since many borrowers are managing both at the same time.

Student loan deferment allows borrowers to pause payments on qualifying federal student loans, including Perkins loans in some cases. Depending on the deferment type, interest may be interest free on subsidized balances, while other loans may still accrue unpaid interest. Deferment time and eligibility vary depending on the reason you qualify. Common qualifying events include enrollment at least half time, active duty military service, National Guard activation, Peace Corps service, or meeting criteria tied to economic hardship, the Supplemental Nutrition Assistance Program, or your state’s poverty guidelines.

Student loan forbearance, by contrast, typically permits a pause or reduced payments for up to 12 months, but interest continues to accrue and you may be charged interest on both federal and private loans. A student loan servicer may grant forbearance when you are experiencing financial hardship, financial trouble, illness, or other temporary setbacks.

Both options are handled through federal loan servicers and require an application process. Before requesting forbearance, look closely at how much unpaid interest could build during the pause. While your request is under review, continue making payments if possible to avoid default.

If you are juggling a mortgage loan, a personal loan, and student loans at the same time, speak with each loan servicer about how your repayment options line up. The relief available can vary depending on the loan type and the specific qualifying event involved.

Student Loan Help is available from Credit.org.

When used wisely, forbearance and deferment can help you protect your home and your finances. But they come with rules and consequences; especially when interest continues to accrue. Always talk to your loan servicer early, understand the repayment terms, and get help if you need it.

Schedule your free housing counseling appointment or call 800-431-8157 to speak with our certified housing counselors today.